Apr 2016

13

BrightPay back with a bang at Accountex 2016

BrightPay is back again at Accountex, 2016. Accountex attracts delegates from the accounting, bookkeeping and financial industry. It is the biggest conference of it’s kind in the UK and BrightPay are delighted to be a part of such an amazing show. Accountex is a free event where delegates benefit from two days of seminars, workshops and networking opportunities. Delegates can even earn free CPD points. What’s not to like? Register here for free tickets.

This year, BrightPay has an even bigger and better stand. The BrightPay team will be conducting one to one live demos where we will be showcasing our payroll, auto enrolment and latest features. BrightPay is a feature packed payroll software tool that offers automatic enrolment functionality included in our licence. There’s no need to fork out extra money for AE modules or add on’s. Save your business money today with BrightPay.

New features for 2016 include the NEST web services / API integration, pre-assessment and post-assessment client reporting, CIS processing, payrolling of benefits, P11D’s, specific import from HMRC’s Basic PAYE Tools and more. Read: What’s new in BrightPay 16/17.

The team will be on hand to answer any questions you have about BrightPay. Live demos will take you through the auto enrolment process, where we enter in a staging date, automatically assess each employee, create and send employee letters, set up a pension scheme and deduct pension contributions and more. BrightPay allows users to prepare enrolment and contribution csv files for upload to 15 pension providers each pay period. View BrightPay’s automatic enrolment features.

With BrightPay, the future is BRIGHT!! For bureaus, BrightPay includes unlimited employees, unlimited employers, automatic enrolment functionality and email & phone support for £199 + VAT / tax year!! This year, exclusively at Accountex NEW customers can avail of 25% off BrightPay 16/17 on the 11th and 12th May only. This Accountex offer is for new customers only for the first year subscription.

Stand number: A520

Apr 2016

11

Increases to UK Statutory Redundancy Pay

There has been an increase from 6th April 2016 in the weekly rate of Statutory Redundancy Pay by £4 from £475 in 2015-16 to £479 in 2016-17. This increase is due to The Employment Rights (Increase of Limits) Order 2016. The maximum compensatory award has also been increased from £78,335 to £78,962.

These increases are only in England, Scotland and Wales. Northern Ireland is governed by different legislation and any revisions on limits by The Employment Rights (Increase of Limits) Order (Northern Ireland) 2016 came into effect on 14th February 2016.

The rates for England, Scotland and Wales displayed on GOV.UK are currently the old rates and this information should be updated soon.

Apr 2016

11

Further Guidance for Employers Re: Employment Allowance

Single-director companies will not be eligible to claim the National Insurance Contributions Employment Allowance for the new tax year 2016-17. The employment allowance for the new tax year 2016-17 will be £3,000, an increase from £2,000 from 2015-16.

Employment Allowance Guidance to changes from 6th April 2016:

• If the only employee is a director of a limited company and paid wages above the Secondary Threshold for Class 1 National Insurance contributions the Employment Allowance will no longer be eligible for claiming. The Secondary Threshold is £156 per week for 2016-17.

• If there is a limited company with a number of employees and a director is one of these employees where the director is the only employee to be paid over the Secondary Threshold, the limited company can no longer claim the Employment Allowance.

For 2016-17 if you are not eligible to claim the Employment Allowance you must not claim it and ensure that the full amount of employer Class 1 National Insurance contributions are paid.

If throughout the 2016-17 tax year the circumstances of the limited company change where more than one employee or director is paid wages above the Secondary Threshold, the company will be able to claim the Employment Allowance for the full tax year. Such companies include where:

1. All employees are directors where they both are paid wages above the Secondary Threshold

2. The directors that are employed are husband and wife and both are paid wages above the Secondary Threshold

3. If seasonal employees are employed and one or more employees are paid wages above the Secondary Threshold in a week

4. If the employee is the only UK based worker of an international company and is paid wages above the Secondary Threshold in a week and meets the other eligibility criteria.

Basically the eligibility to claim the Employment Allowance is determined on if the additional employee is paid wages above the Secondary Threshold of £156 in 2016-17 or directors must be paid above the Annual Secondary Threshold of £8,112 or on a pro-rata basis if the directorship commenced after the start of the tax year.

Apr 2016

7

BrightPay at the TaxAssist Conference

BrightPay are delighted to be exhibiting at this year’s TaxAssist Conference. The annual conference will be held at the Celtic Manor Resort in Newport, Wales and will see almost 350 delegates partake in a day of seminars, business, networking and entertainment.

The day will kick off with an exhibition in the morning showcasing 40 exhibitors, including BrightPay. After a buffet lunch, delegates will benefit from presentations by Tax Assist Directors and table discussions with key partners of the franchise.

As a preferred payroll supplier to TaxAssist Accountants, BrightPay’s Managing Director Paul Byrne will hold one of the table discussions. Paul will discuss ‘A Simple Strategy to Automate Auto Enrolment’ which will outline how accountants can automate AE to improve profitability.

BrightPay payroll and auto enrolment software enables accountants to streamline auto enrolment tasks, improving efficiency and profitability. Visit BrightPay’s stand to avail of a demo of the software.

BrightPay’s bureau licence includes unlimited employers, unlimited employees, free support and full auto enrolment functionality. BrightPay 2016/17 includes a number of new features, including integrated CIS & P11D functionality – find out more here.

Read: What happens if you don't comply with automatic enrolment?

Apr 2016

4

What happens if you don't comply with automatic enrolment?

There are a number of duties that employers need to undertake to comply with automatic enrolment. Even if there are no eligible job holders, certain steps need to be followed. The responsibility of auto enrolment does rest with the individual employer. If an employer fails to comply the Pensions Regulator (TPR) will take action. They may issue you with a notice or penalty.

TPR will enforce penalties if the employer chooses to ignore their automatic enrolment duties. The enforcement action starts with statutory notices being issued to the employer. This is then followed by penalty notices and further non-compliance may lead to court action. TPR does want to work with employers to make sure they understand their employer duties.

In certain circumstances, where the employer genuinely did not understand their duties or due to unforeseen circumstances have not been able to comply, TPR will work with the employer to ensure compliance. However, those who do not carry out the AE duties in accordance with the law will face enforcement action and penalties.

Enforcement Action

The Pensions Regulator will investigate willful and non-willful non-compliance. They are within their rights to carry out inspections and request certain information from employers. TPR will enforce non-compliance in a number of ways:

• Informal action: TPR will correspond with the employer to issue guidance and help by telephone, email, letter and in person. The employer may be issued with a warning letter giving them a specific amount of time to become compliant with their AE duties.

• Statutory notice: TPR can issue statutory notices informing the employer that they must comply with their AE duties. The employer could also be directed to pay any contributions they have missed or were late in paying. TPR does then have the authority to estimate and charge interest on unpaid contributions which the employer must pay in addition to the missed contribution payments.

• Penalty notice: TPR has further authority to issue employers with penalty notices penalising deliberate and intentional non-compliance. If an employer fails to comply with instructions as per their statutory notice or if the employer deliberately breaks the law then a fixed penalty will be issued. The penalty notice is fixed at £400 to be paid within a certain time period.

• Escalating penalty notice: TPR can issue the employer with an escalating penalty notice for failing to comply with a statutory notice. If the employer receives this penalty notice they will be penalized with a daily rate of between £50 and £10,000. The value of the penalty depends on the number of employees an employer has.

• Civil penalty notice: TPR can issue a civil penalty notice when an employer fails to pay the contributions that are outstanding. If the employer receives this notice there are heavy penalties of up to £5,000 for individuals and up to £50,000 for organisations.

• Prohibited recruitment conduct penalty notice: Employers can be issued with a prohibited recruitment conduct penalty notice when an employer fails to comply with a compliance notice or if it is evidence of a breach. Depending on the number of employees, the penalty has a rate ranging from £1,000 to £5,000. TPR aims to fully recover all penalties that are issued.

Receiving a penalty notice

Employers can pay their penalties using TPR's online payment service. Employers will need their penalty notice reference which is located on the front of the notice. It will be important to pay the penalty by the date displayed on the penalty notice. Failure to pay will result in the Regulator bringing formal legal proceedings against the employer to recover the penalty amounts. Failure to comply and pay penalties could result in criminal prosecution.

Legal Proceedings

TPR has the right to take civil action through the courts to recover penalties against employers. If the employer intentionally and willfully fails to comply with their auto enrolment duties, they may be prosecuted. TPR also has the right to confiscate goods where there is a criminal conviction and restrain assets during criminal investigations.

How to appeal

TPR allows employers to apply for a review if they have been issued with a notice. Employers must submit an application with supporting evidence within 28 days of the notice being issued. The Regulator will then inform the employer when a decision can be expected.

Employers can apply for a review once they receive any of the following notices or penalties; compliance notice; unpaid contributions notice; third party compliance notice; fixed penalty notice; escalating penalty notice; prohibited recruitment compliance notice or prohibited recruitment penalty notice. You can apply for a review online, by post, by telephone or in person. Visit TPR website for more info.

Avoid Penalties & Fines

Make sure you are prepared for your automatic enrolment duties. The Pensions Regulator advises employers and payroll bureaus to utilise payroll software that can cater and automate auto enrolment duties. It would be advisable to check that your current payroll system is compatible with your chosen pension scheme.

Book a demo with BrightPay to see just how easy and straightforward auto enrolment can be. A quick 15/20 minute demo will show you how we enter in a staging date, assess each employee, send employee letters, set up a pension scheme and deduct pension contributions. Our latest feature allows payroll you to create a pre-assessment overview of AE before the staging date is reached. View a full list of BrightPay's auto enrolment features.

Apr 2016

4

Preparing for your move to BrightPay - Useful Guidance

Moving from one payroll software to another can sometimes be a daunting task, but with preparation this needn't be.

To help with this preparation, we have put together the following guidance to assist you with the migration to BrightPay from a previous payroll software:

Check if your current software allows the exporting of employee information

BrightPay facilitates the importing of employee information in CSV format. Therefore if your current payroll software allows the export of employee information in CSV format (or to Excel, which can subsequently be converted to CSV format), BrightPay's import utility can be used. Should your current payroll software not allow the export of employee information, then employee details will need to be set up manually within BrightPay.

Allow yourself enough time

It is important to allow yourself enough time to perform an import before your next payroll run is due for the company. Performing the import well in advance of your next payroll due date will allow you to review and check the employee data you have brought in and also to manually enter in additional employee information, if required.

Allowing yourself enough time is also particularly important if you are required to manually set up your employees (and if applicable their mid-year cumulative pay information), due to your current payroll software not allowing the export of employee data.

Choose a convenient time to migrate to BrightPay

For most companies, the easiest time to migrate to a new payroll software is at the start of a new tax year, as this only requires the importing of employee details. As employees will start the new tax year with zero balances, there is no requirement to import across mid-year cumulative pay information.

If migrating to BrightPay at the start of the tax year isn't viable, then an import of both employee and their mid-year pay information can be performed in BrightPay at any point in the tax year (should your current software allow the export of such information). If migrating to BrightPay mid-year, then it may be more convenient to perform this task after a tax period end, to avoid split P32 records. Make sure to select the option 'Continue Partway in the Tax Year' when setting up your employer details in BrightPay, to facilitate the mid-year import.

Familiarise yourself with BrightPay's terminology

Payroll software providers can often differ slightly on the terminology they use within their software - for example, what is known as 'works number' in BrightPay may be known as 'employee number' in another payroll software. Before performing a CSV import into BrightPay, it is therefore recommended to familiarise yourself with the terminology used in BrightPay and to find its equivalent in your existing software, if different. This will assist at the import stage, when matching columns to the data it represents. Please click here to view a list of the terminology used in BrightPay.

Still have access to your previous software at time of import into BrightPay

It is advisable to still have access to your previous payroll software when performing your migration to BrightPay - this is in case you need to create a new export file in your previous software (for example, employee data hasn't exported out correctly, mid-year totals are for the wrong period etc.) or you wish to cross-check employee data after import. If your previous software licence has expired and a new export file is needed, you may be left with having to manually set up your employee information.

Run a parallel payroll with your previous software

If you do still have access to your previous software, then a useful exercise is to run both your old payroll system and BrightPay side-by-side for a period of time. This is a good way to determine that everything has been set up correctly in BrightPay and there are no inaccuracies.

Important note: if running parallel pay runs, ensure that only one RTI submission is submitted, from either your old or new system.

Follow BrightPay's dedicated support documentation

BrightPay currently has dedicated support documentation to assist you with migrating to BrightPay from SAGE, IRIS, Moneysoft and HMRC Basic PAYE Tools.

If you are migrating from another payroll software, please refer to our support documentation on Importing using a CSV File - Other Software and Importing using an FPS File - Other Software

Mar 2016

31

Budget 2016 - Employer Focus

The main points to be noted by employers from Budget 2016 announced by Chancellor George Osborne are:

• The personal tax allowance will increase by £500 from £11,000 to £11,500 from April 2017

• The higher rate tax threshold will increase to £45,000 from April 2017

• Termination payments over £30,000 which are subject to income tax currently from April 2018 will be subject to Employer National Insurance Contributions (NICs)

• Class 2 National Insurance Contributions for self-employed people will be scrapped from April 2018

• The range of benefits that are subject to income tax and National Insurance Contributions are going to be examined by the government with the aim of limiting the range of benefits subject to income tax and NIC. It is the view of the government that such benefits such as the pension saving, childcare and schemes such as the Cycle to Work will still continue to benefit from the relief of income tax and NIC when provided through salary sacrifice agreements.

• A new discount rate for employers contribution to the unfunded public service pension schemes is set at 2.8% and in 2019-20 employers will have to pay higher contributions into the scheme as a result.

• The rate of tax on loans to directors and participators will increase by 7.5% to 32.5% in April 2016.

Mar 2016

23

BrightPay 2016/17 is Now Available. What's New?

BrightPay 2016/17 is now available (for new customers and existing customers). Here’s a quick overview of what’s new:

2016/17 Tax Year Updates

- 2016/17 rates, thresholds and calculations for PAYE, National Insurance contributions, Student Loan deductions, Statutory Sick Pay, Statutory Maternity Pay, Statutory Adoption Pay, Statutory Paternity Pay, and Statutory Shared Parental Pay.

- The emergency tax code has changed from 1060L to 1100L. When importing from BrightPay 2015/16, L codes are uplifted by 40, while M codes are uplifted by 44 and N codes by 36.

- Full support for Scottish Rate of Income Tax (SRIT) codes.

- The new NI category H is available for apprentices under 25 in qualifying circumstances. Payments to class H employees are not liable to Class 1 secondary NICs.

- With the abolishment of Contracted Out Pension, HMRC have discontinued NI categories D, E, K, I and L. When importing from BrightPay 2015/16, employees in any of these categories are moved into the equivalent non-contracting-out category.

- Support for Plan 1 and Plan 2 Student Loan deductions.

- Ability to process 2016/17 coding notices.

- Eligible employers can continue to claim the £3,000 Employment Allowance which can be used to reduce Employer Class 1 Secondary NICs payments to HMRC.

- Updated P11, P45, P60, P30 and P32 forms.

- Updated RTI submissions in line with the latest HMRC specifications. BrightPay continues to be officially HMRC Recognised for all RTI submission types.

Expenses and Benefits

BrightPay 2016/17 allows you to record all types of reportable expenses and benefits that you provide to your employees:

- Assets transferred (cars, property, goods or other assets)

- Payments made on behalf of employee

- Tax on notional payments

- Vouchers and credit cards

- Living accommodation

- Mileage allowance and passenger payments

- Car and fuel

- Vans and fuel

- Private medical treatment or insurance

- Qualifying relocation expenses payments and benefits

- Services supplied

- Assets placed at the employee’s disposal

- Other items (Class 1A)

- Other items (Non-Class 1A)

- Income Tax paid but not deducted from director’s remuneration

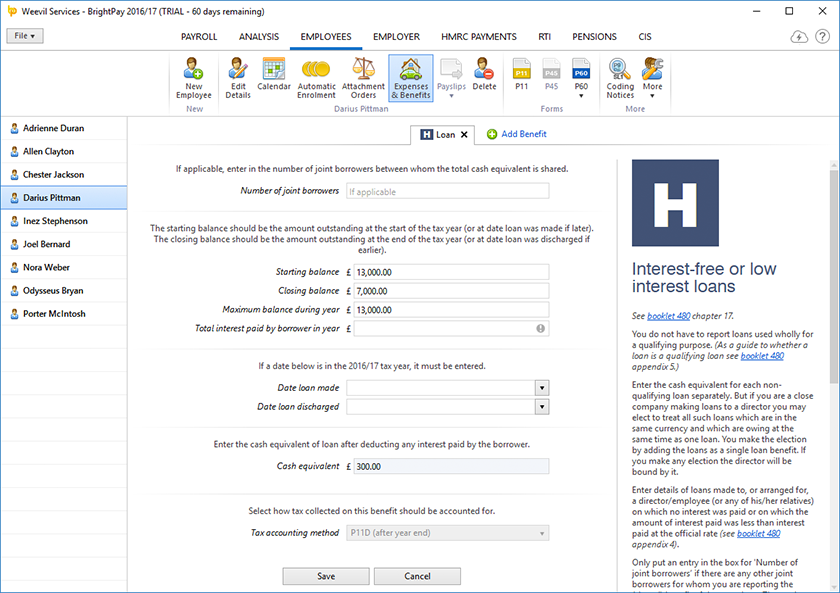

- Interest-free or low interest loans

- Travelling and subsistence payments

- Entertainment

- General expenses allowance for business travel

- Payments for use of home telephone

- Non-qualifying relocation expenses

- Other expenses

BrightPay can produce a P11D for sending to HMRC after year end which includes your Class 1A NICs declaration and details of the expenses and benefits provided including cash equivalents.

If you register for payrolling of benefits by 5 April 2016, BrightPay 2016/17 also supports calculating the PAYE on expenses and benefits in each pay period.

We will be back-porting some of the expenses and benefits features to BrightPay 2015/16 to allow you to send your P11D for the 2015/16 tax year. Look out for an upgrade in April/May.

Note: Expenses/benefits and P11D are not available for Free Licence customers.

Construction Industry Scheme (CIS)

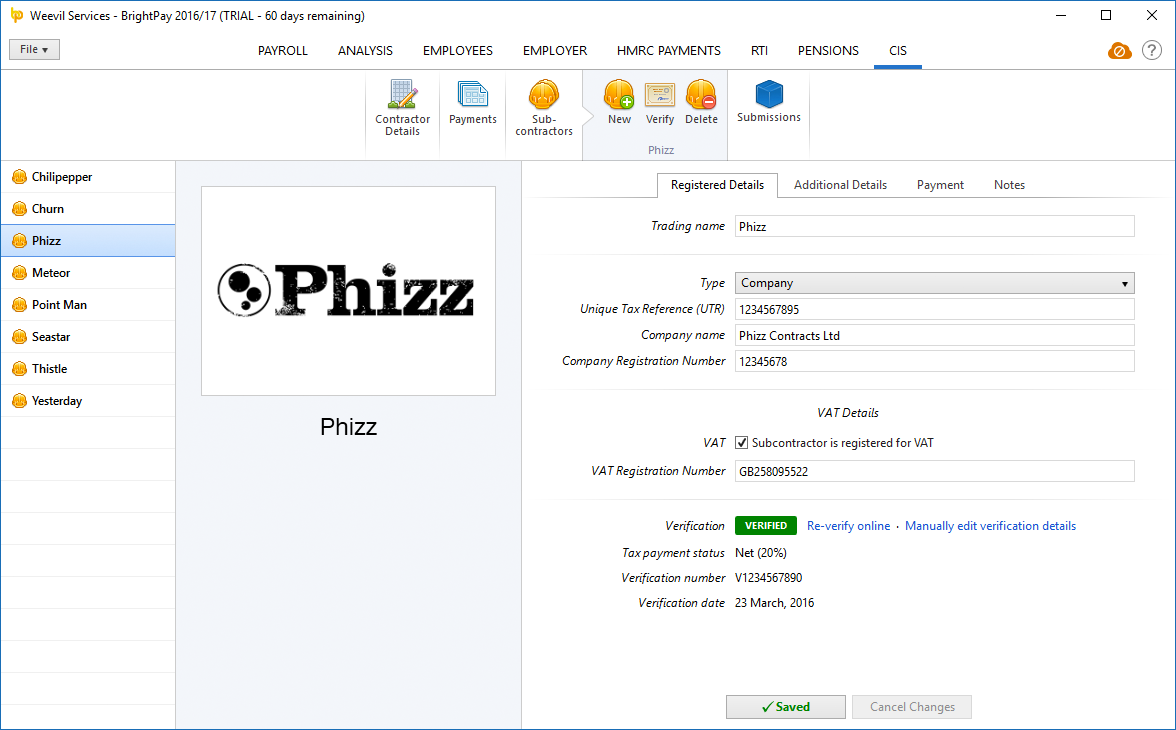

BrightPay 2016/17 has full support for paying subcontractors under the Construction Industry Scheme (CIS):

- Add/edit subcontractors, or import from CSV.

- Pay subcontractors tax weekly or tax monthly (all year or part year).

- Customisable basic pay, daily rates, hourly rates, additions, deductions, etc.

- Record cost of materials and VAT.

- Calculate CIS deduction amounts according to subcontractor's tax payment status.

- Print, export to PDF, or email Subcontractor Payment and Deduction Statements.

- Send CISREQ subcontractor verification submissions and apply response data.

- Send CIS300 monthly returns.

- BrightPay tracks the number of unsent CIS submissions, similar to RTI.

- Report on CIS data in BrightPay Analysis (some built-in CIS reports are available)

Note: CIS is not available for Free Licence customers.

Pensions and Automatic Enrolment

If you have not yet entered your Automatic Enrolment Staging Date in BrightPay, you can now connect directly to the Pensions Regulator and retrieve it automatically from within BrightPay.

BrightPay 2016/17 now tracks the number of enrolment/contributions submissions that you have not yet submitted to your pension scheme provider. The number is shown on the main PENSIONS tab, and contributes to the total number shown on the Open Employer screen (which also includes RTI and CIS).

We'll be continuing to update Automatic Enrolment during the 2016/17 tax year and provide dedicated support for more pension scheme providers.

Coming Soon: BrightPay Cloud

BrightPay Cloud will allow you to connect your BrightPay employer data to a web based service that provides:

Secure Online Backup

Automatically backs up your BrightPay data to the cloud. A historical set of backups is maintained. Your data file can be restored from an online backup at any time.

Employee Self-Service

Enables employees to log in to a web-based portal using their PC, Mac or smartphone to retrieve payslips, view their calendar, request annual leave, view/update personal information, and more.

Bureau Client Self-Service

Enables payroll bureaux to provide an online portal not only for their customer's employees (i.e. employee self-service as described above), but also an employer portal for direct use by their employer customers, enabling them to view payroll reports, P30s, calendar, all employee information, and more.

BrightPay Cloud will work directly with BrightPay 2016/17, but also allow you to upload your BrightPay 2015/16 data to immediately have a full year of historical data to power the self-service features.

BrightPay Cloud will cost £49 per employer per tax year (with discounted bulk pricing for bureaux also available).

We'll have more news very soon. As a BrightPay customer, you'll be the first to know. Watch this space!

Other 2016/17 Changes in BrightPay

- Ability to import employees from an FPS XML file.

- When importing from HMRC Basic PAYE Tools, you can choose to do so from the previous tax year or the current tax year.

- Pension-able gross can be split into separate employee and employer pension-able gross amounts.

- Basic pay, daily pay and hourly pay can now be explicitly flagged as liable/not-liable to PAYE, NICs, employee pension, and employer pension.

- Additional Statutory Paternity Pay is no longer relevant and is removed in BrightPay 2016/17.

- The NIC Upper Accrual Point is no longer relevant and is removed from BrightPay 2016/17.

- New wider range of built-in reports.

- Pension provider enrolment/contributions submissions and file formats have been updated to the latest versions.

- Ability to view submission logs for NEST web service submissions.

- An HMRC payment date is no longer required to be able to progress to the next HMRC pay period. Any pay period can be clicked into at any time.

- Ability to report on HMRC payment amounts in Analysis.

- Employee passwords can be randomly generated.

- Lots of minor improvements throughout the entire BrightPay user interface, as well as the latest bug fixes.

BrightPay 16/17 is the same price as BrightPay 15/16 (including FREE for small employers with up to three employees). Support will continue to be free of charge for all users.

Mar 2016

17

Late Filing Relaxation of FPS to end on 5th April 2016

Penalties from HMRC will be issued if any late filing of a Full Payment Submission (FPS) from 6th April 2016 onwards.

Currently there is a 3 day relaxation for filing a late Full Payment Submission which is detailed per the HMRC website GOV.UK https://www.gov.uk/guidance/what-happens-if-you-dont-report-payroll-information-on-time

"HMRC won’t charge a penalty if:

• your FPS is late but all reported payments on the FPS are within 3 days of your employees’ payday (this applies from 6 March 2015 to 5 April 2016)"

The other circumstances where HMRC will not issue a penalty for late submission of an FPS are when:

• you’re a new employer and you sent your first FPS within 30 days of paying an employee

• it’s your first failure in the tax year to send a report on time (this doesn’t apply to employers who register with HMRC as an annual scheme or have fewer than 50 employees for the tax year 2014 to 2015)

Mar 2016

17

Increase in National Minimum Wage from 1st October 2016

The Low Pay Commission's (LPC) recommendations for the rates of the minimum wage for employees under 25 and apprentices has been accepted by the Government and this take effects from 1st October 2016.

These include:

21-24 year olds £6.95 per hour an increase of 3.7%

Youth Development Rate - 18-20 year olds £5.55 per hour an increase of 4.7%

16-17 Year Old Rate £4.00 per hour

Apprentice Rate £3.40 per hour an increase of 3%

The Government has introduced the National Living Wage of £7.20 per hour for employees over 25 which takes effect on 1st April 2016.